Health Insurance for Seasonal Workers: Your Options, Explained

Let's be honest — the American healthcare system was not designed with seasonal workers in mind. The enrollment windows, the state-by-state rules, the income thresholds that shift every few months — it's genuinely confusing, and that confusion has real consequences. Uninsured gaps, surprise bills, coverage that evaporates the moment your season ends.

If you've ever let your insurance lapse and just hoped nothing went wrong, you're not alone. Most seasonal workers have. The problem isn't that you're irresponsible — it's that the system assumes a different type of stability that your life may not have.

This guide breaks down your real options as a seasonal outdoor worker: what they are, when they apply, and how to make a decision without spending a week reading government websites.

Why Health Insurance Is Different for Seasonal Workers

Standard healthcare advice assumes one employer, one state, one steady income. For river guides, ski instructors, outdoor educators, and anyone else living and working seasonally, that's just not the reality.

As a seasonal worker, you might:

Earn $20–70K over six months and very little the rest of the year

Split your time between Utah winters and Colorado summers

Work for an employer that offers coverage October through April — and nothing after

Cross the Medicaid income threshold multiple times in a single year

Your income and state of residence both determine what you qualify for, what it costs, and where you can actually get care. The system can work for you — it just requires more intentionality than it does for someone in a salaried 9-to-5.

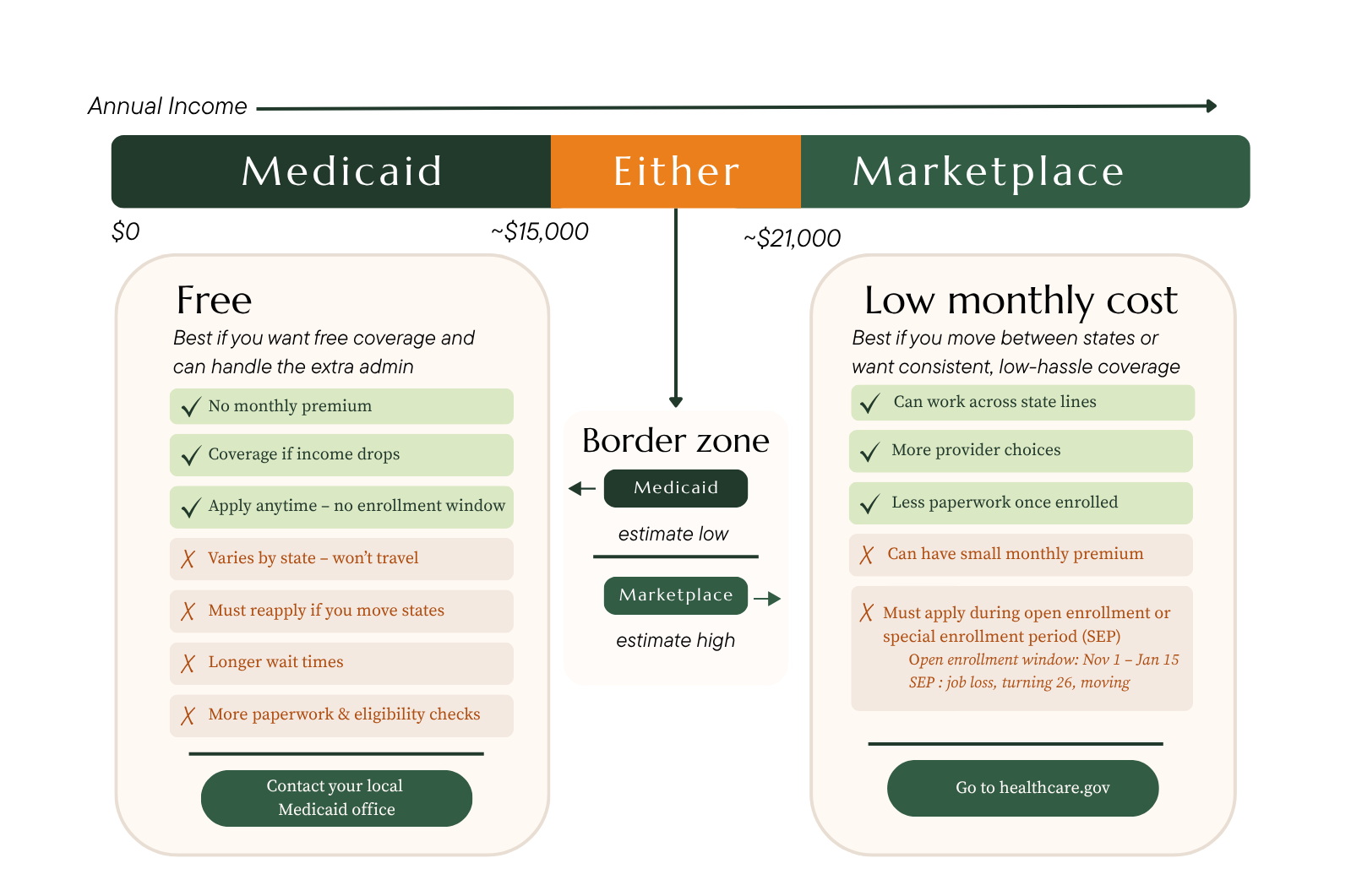

Medicaid vs. Marketplace: Which Is Right for Seasonal Workers?

Most seasonal workers end up on one of two paths: Medicaid or an ACA Marketplace plan through healthcare.gov. Understanding the difference is the foundation of everything else.

Medicaid is free (or very low cost) coverage available to people below a certain income threshold — roughly $1,800/month for a single adult, though this varies by state. There's no monthly premium, no enrollment window, and you can apply any time of year. The tradeoff: Medicaid is state-specific. Move states and you lose it. More paperwork, more eligibility checks. But if your income drops between seasons, it's one of the most valuable tools available to you.

ACA Marketplace plans are private insurance plans with income-based subsidies that can significantly reduce your monthly cost. These plans work across state lines, which matters when you're splitting your year between regions. The catch: you can only enroll during specific windows (open enrollment or a qualifying life event), and there's typically a monthly premium involved.

There's also a "border zone" that seasonal workers fall into more than most: the income range where you might qualify for either, depending on when in the year you apply. When income is low (off-season), Medicaid may be the right call. When income is higher (peak season), a Marketplace plan often makes more sense. Neither is inherently better — what matters is knowing where your income sits and acting on it.

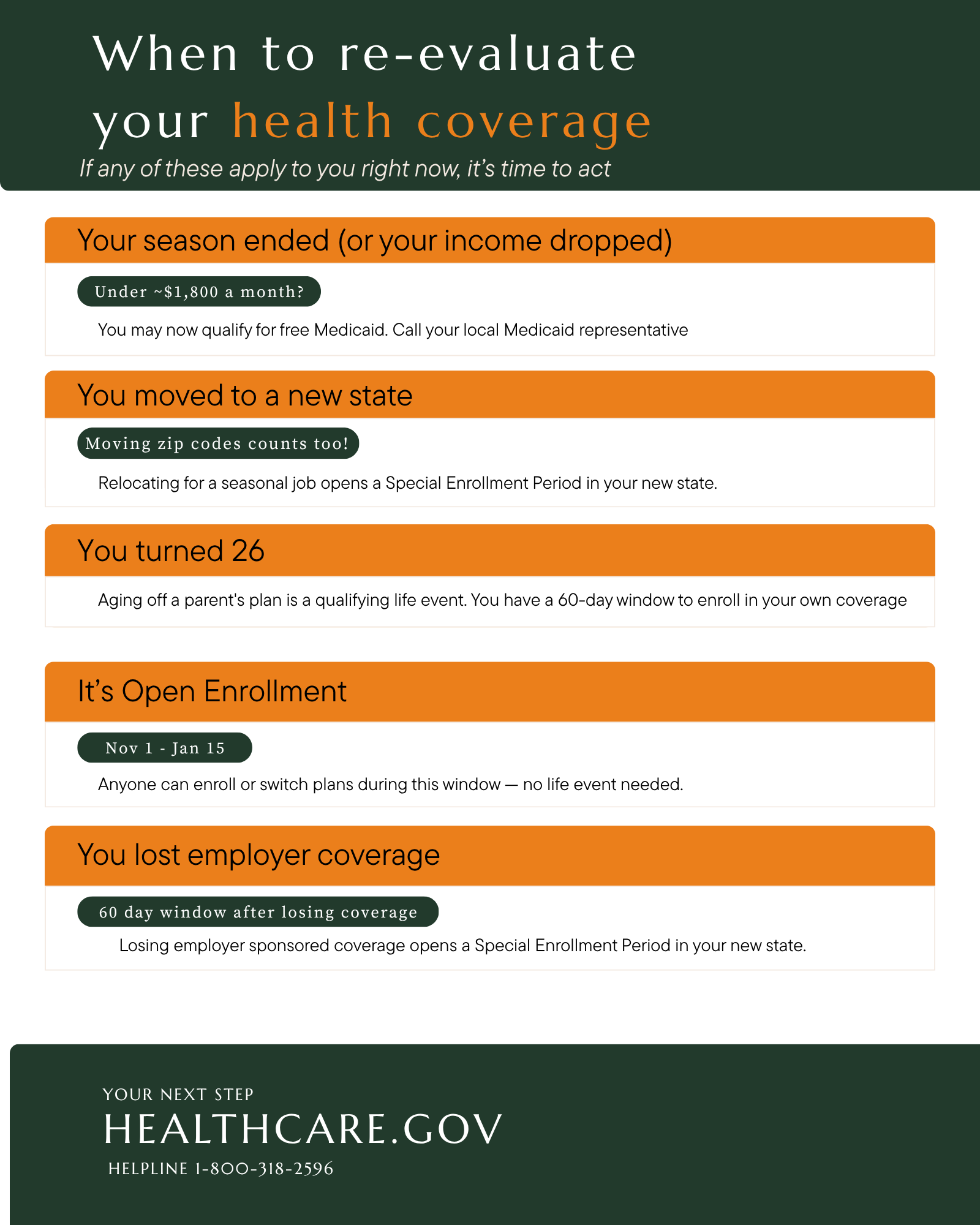

When to Re-Evaluate Your Health Coverage

The biggest mistake seasonal workers make isn't choosing the wrong plan. It's not acting fast enough when their situation changes.

These are the moments that should trigger an immediate coverage review:

Your season ended or your income dropped. If you're now earning under ~$1,800/month, you may qualify for free Medicaid. Call your local Medicaid office or start at healthcare.gov.

You moved to a new state. Even a new zip code counts. Relocating for a seasonal job opens a Special Enrollment Period — a window to enroll in coverage without waiting for open enrollment.

You turned 26. Aging off a parent's plan is a qualifying life event. You have 60 days to get your own coverage. That window closes whether or not you remember it.

It's Open Enrollment (Nov 1 – Jan 15). Anyone can enroll or switch plans during this window — no life event required. Use it as your annual reset.

You lost employer coverage. This opens a 60-day Special Enrollment Period. Don't wait for a "good time" to deal with it — the clock starts the day your coverage ends.

Your Health Coverage Checklist for Seasonal Workers

Not sure where to start? Begin here:

Know your monthly income range. Under or over ~$1,800/month is your first fork in the road between Medicaid and Marketplace.

Identify your trigger. Did you just lose coverage, move states, turn 26, or end a season? You may have an enrollment window open right now.

Start at healthcare.gov. Even if you think you might qualify for Medicaid, healthcare.gov will route you correctly. You don't need to have the answer before you show up.

Call for free help. Every state has free enrollment navigators. Marketplace helpline: 1-800-318-2596.

Get Organized Before the Next Transition

Understanding your options is step one. Building a system that keeps you from scrambling every time your season shifts — that's step two.

The Shoulder Season Series is a four-week program built specifically for outdoor and seasonal workers who want to get their finances, health coverage, and career clarity dialed in before the next chapter starts. Week 3 is dedicated entirely to health and wellness systems — including a deep dive on exactly this: how to figure out your coverage situation, what to do when life transitions happen, and how to stop letting healthcare be the thing that falls through the cracks. If you want a structured space to actually work through this stuff (and not just read about it), that's where to start.